Research

By clicking the images below you can download the public versions of Rewheel's latest studies and of selected older studies. Send us an email if you wish to purchase the PRO version of a study or wish to subscribe to Rewheel's annual research service.

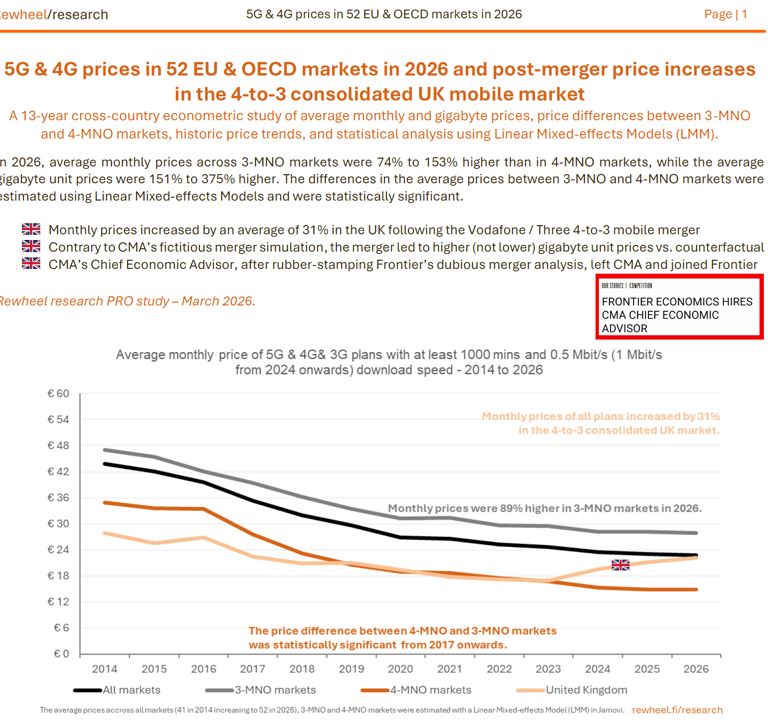

In 2026, average monthly prices across 3-MNO markets were 74% to 153% higher than in 4-MNO markets, while the average gigabyte unit prices were 151% to 375% higher. The differences in the average prices between 3-MNO and 4-MNO markets were estimated using Linear Mixed-effects Models and were statistically significant. Monthly prices increased by an average of 31% in the UK following the Vodafone / Three 4-to-3 mobile merger. Contrary to CMA’s fictitious merger simulation, the merger led to higher (not lower) gigabyte unit prices vs. counterfactual. CMA’s Chief Economic Advisor, after rubber-stamping Frontier’s dubious merger analysis, left CMA and joined Frontier.

5G & 4G prices in 52 EU & OECD markets in 2026 and post-merger price increases in the 4-to-3 consolidated UK mobile market

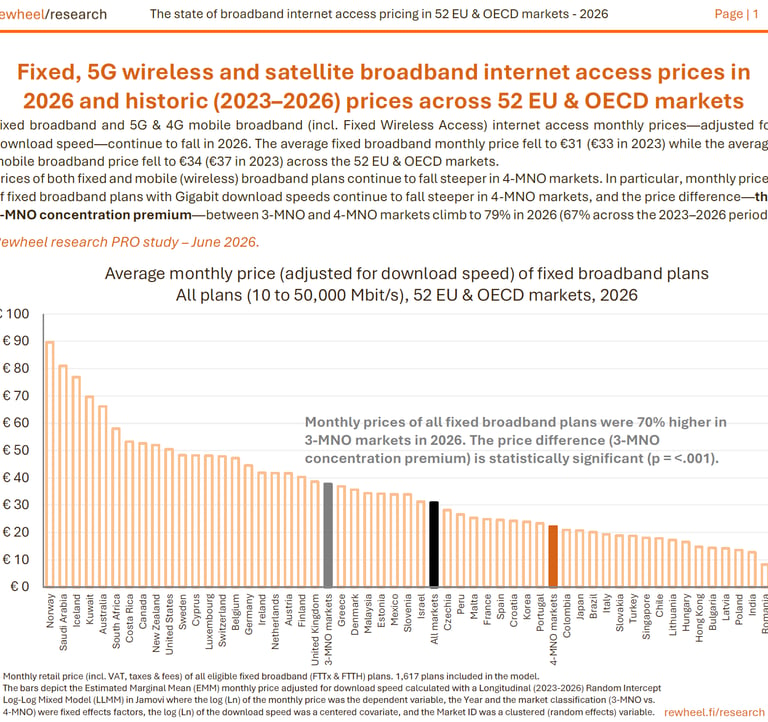

Fixed, 5G wireless and satellite broadband internet access prices in 2026 and historic (2023–2026) prices across 52 EU & OECD markets

Fixed broadband and 5G & 4G mobile broadband (incl. Fixed Wireless Access) internet access monthly prices—adjusted for download speed—continue to fall in 2026. The average fixed broadband monthly price fell to €31 (€33 in 2023) while the average mobile broadband price fell to €34 (€37 in 2023) across the 52 EU & OECD markets. Prices of both fixed and mobile (wireless) broadband plans continue to fall steeper in 4-MNO markets. In particular, monthly prices of fixed broadband plans with Gigabit download speeds continue to fall steeper in 4-MNO markets, and the price difference—the 3-MNO concentration premium—between 3-MNO and 4-MNO markets climb to 79% in 2026 (67% across the 2023–2026 period).

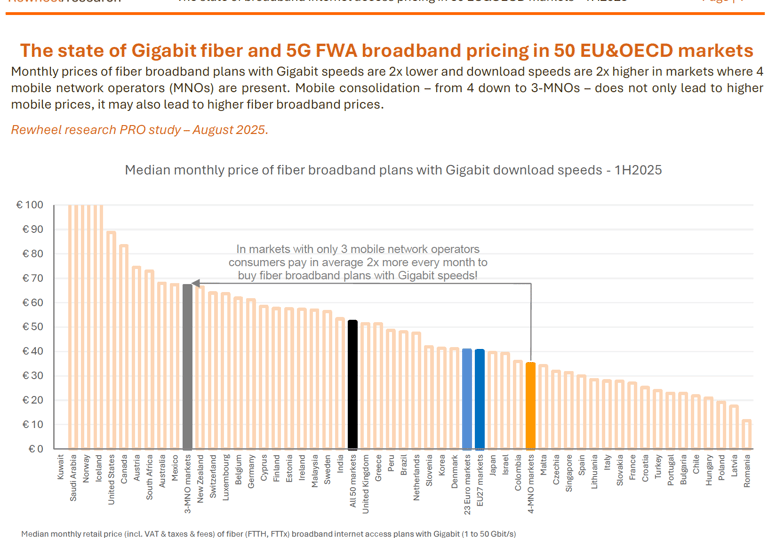

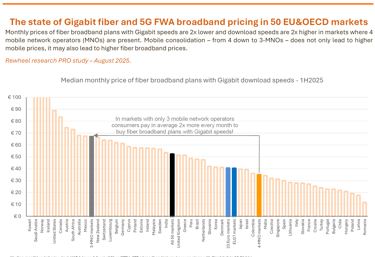

The state of Gigabit fiber & 5G FWA broadband pricing in 50 EU&OECD markets - 1H2025

Monthly prices of fiber broadband plans with Gigabit speeds are 2x lower and download speeds are 2x higher in markets where 4 mobile network operators (MNOs) are present. Mobile consolidation – from 4 down to 3-MNOs – does not only lead to higher mobile prices, it may also lead to higher fiber broadband prices.

The state of 5G&4G pricing in 50 EU&OECD mobile markets - 1H2025

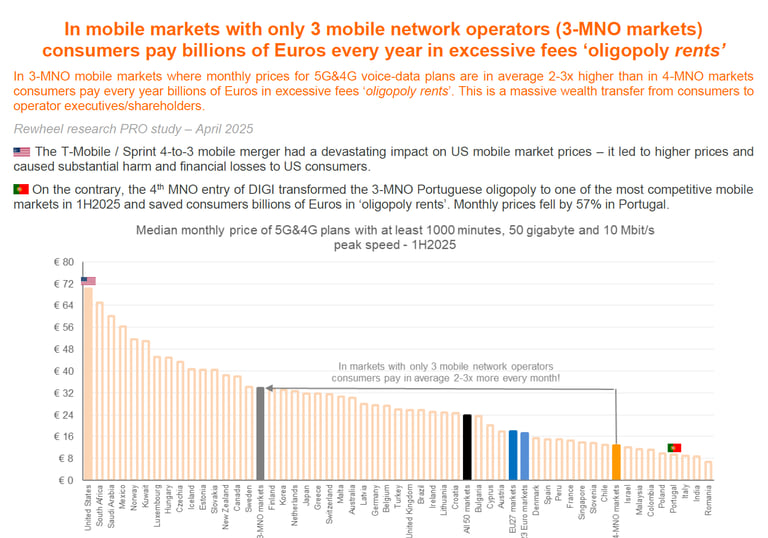

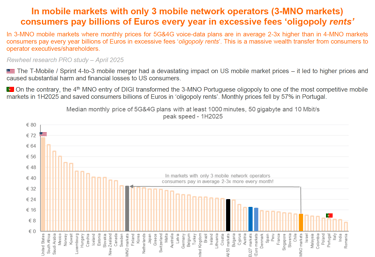

In markets with only 3 mobile network operators (3-MNO markets) where monthly prices for 5G&4G voice-data plans are in average 2-3x higher than in 4-MNO markets consumers pay every year billions of Euros in excessive fees ‘oligopoly rents’. This is a massive wealth transfer from consumers to operator executives/shareholders.

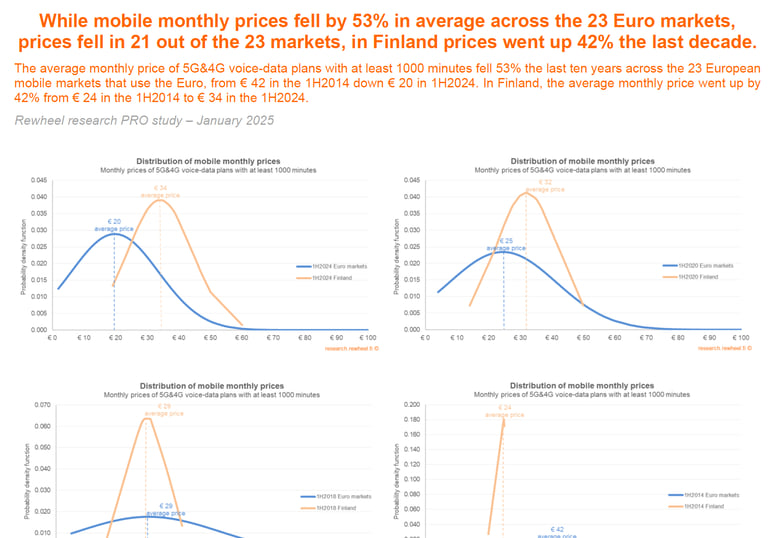

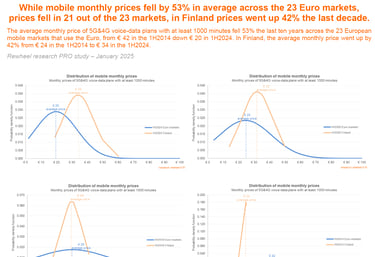

While mobile monthly prices fell by 53% in average across the 23 Euro markets, prices fell in 21 out of the 23 markets, in Finland prices went up 42% the last decade. The average monthly price of 5G&4G voice-data plans with at least 1000 minutes fell 53% the last ten years across the 23 European mobile markets that use the Euro, from € 42 in the 1H2014 down € 20 in 1H2024. In Finland, the average monthly price went up by 42% from € 24 in the 1H2014 to € 34 in the 1H2024.

Mobile monthly prices in Euro markets fell by 53% the last decade, in Finland prices went up by 42% - 2025

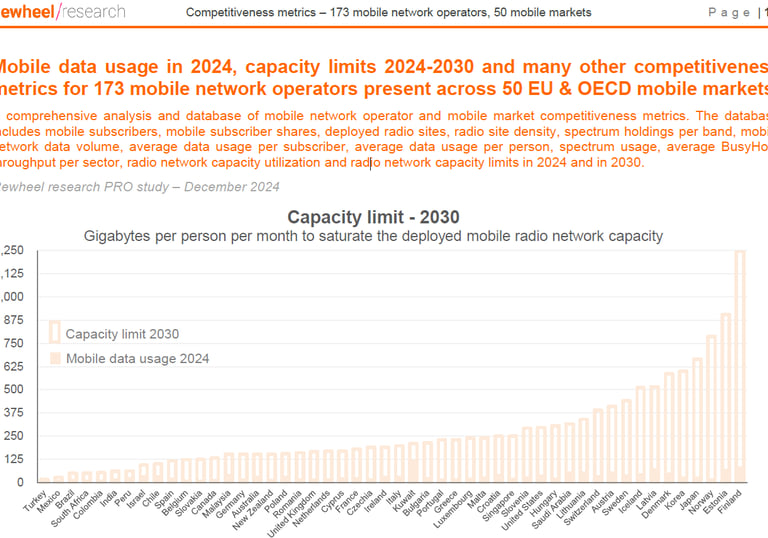

Competitiveness metrics – 173 mobile network operators, 50 mobile markets - 2024

Mobile data usage in 2024, capacity limits 2024-2030 and many other competitiveness metrics for 173 mobile network operators present across 50 EU & OECD mobile markets. The database includes mobile subscribers, mobile subscriber shares, deployed radio sites, radio site density, spectrum holdings per band, mobile network data volume, average data usage per subscriber, average data usage per person, spectrum usage, average BusyHour throughput per sector, radio network capacity utilization and radio network capacity limits in 2024 and in 2030.

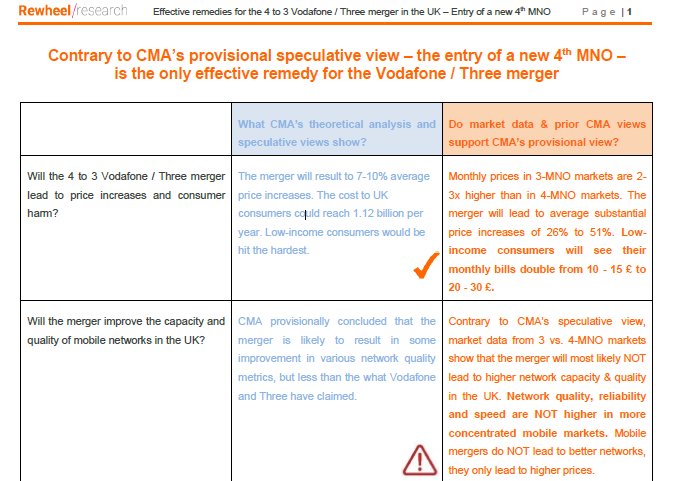

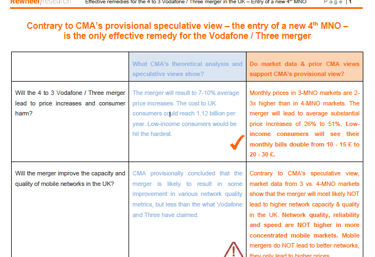

Contrary to CMA’s provisional speculative view – the entry of a new 4th MNO – is the only effective remedy for the Vodafone / Three merger - September 2024

Contrary to CMA’s current speculative view – the entry of a new 4th MNO – is the only effective remedy for the Vodafone / Three merger. The CMA Chief Executive, Alex Chisholm, categorically stated in the open letter he wrote to the European Commission during the 2016 investigation of the 4 to 3 Three / O2 merger in the UK that “Absent of a new 4th MNO entry the only option available to the Commission is prohibition.”.

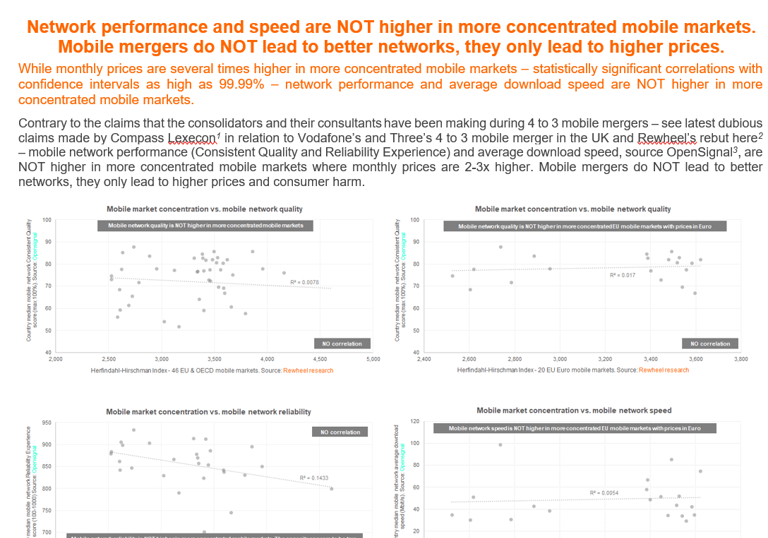

Network performance and speed are NOT higher in more concentrated mobile markets. Mobile mergers do NOT lead to better networks, they only lead to higher prices. While monthly prices are several times higher in more concentrated mobile markets – statistically significant correlations with confidence intervals as high as 99.99% – network performance and average download speed are NOT higher in more concentrated mobile markets.

Network performance and speed are NOT higher in more concentrated mobile markets - September 2024

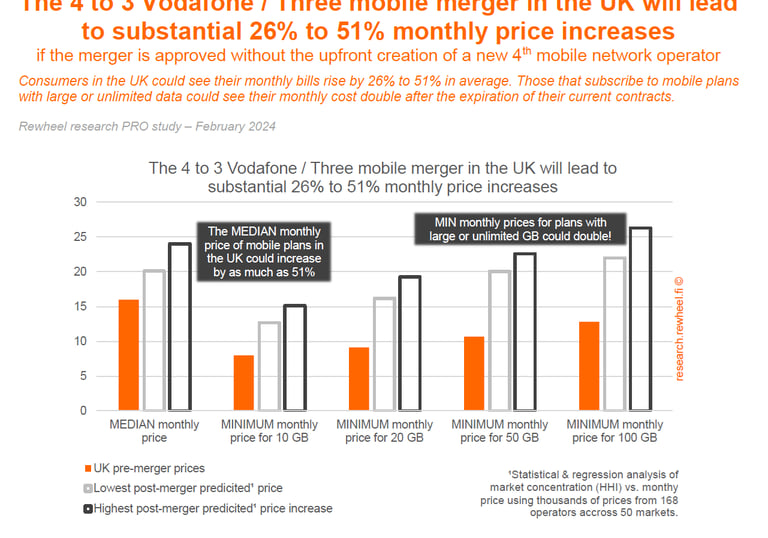

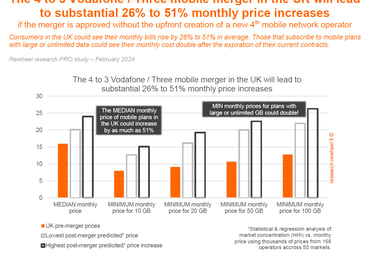

The Vodafone/Three mobile merger in the UK will lead to substantial 26%-51% monthly price increases - 2024

The 4 to 3 Vodafone / Three mobile merger in the UK will lead to substantial 26% to 51% monthly price increases if the merger is approved without the upfront creation of a new 4th mobile network operator Consumers in the UK could see their monthly bills rise by 26% to 51% in average. Those that subscribe to mobile plans with large or unlimited data could see their monthly cost double after the expiration of their current contracts.

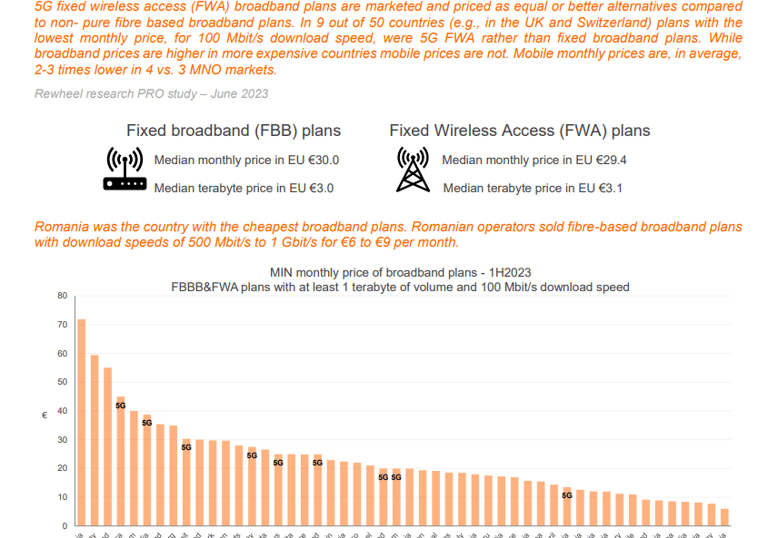

The state of broadband (FBB&FWA) pricing – 1H2023

5G fixed wireless access (FWA) broadband plans are marketed and priced as equal or better alternatives compared to non- pure fibre based broadband plans. In 9 out of 50 countries (e.g., in the UK and Switzerland) plans with the lowest monthly price, for 100 Mbit/s download speed, were 5G FWA rather than fixed broadband plans. While broadband prices are higher in more expensive countries mobile prices are not. Mobile monthly prices are, in average, 2-3 times lower in 4 vs. 3 MNO markets.

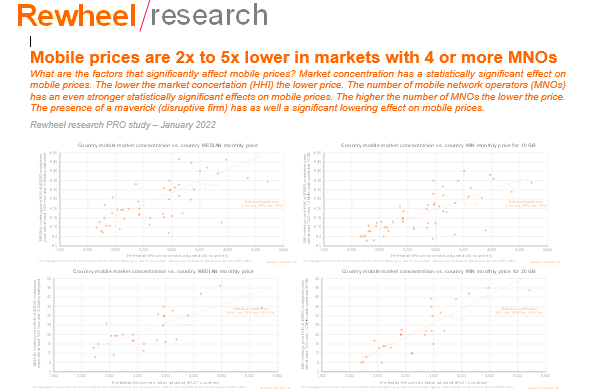

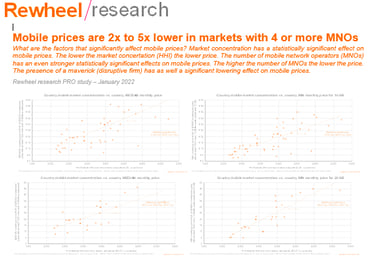

What are the factors that significantly affect mobile prices? Market concentration has a statistically significant effect on mobile prices. The lower the market concertation (HHI) the lower price. The number of mobile network operators (MNOs) has an even stronger statistically significant effects on mobile prices. The higher the number of MNOs the lower the price. The presence of a maverick (disruptive firm) has as well a significant lowering effect on mobile prices.

Mobile prices are 2x to 5x lower in markets with 4 or more MNOs - 2022

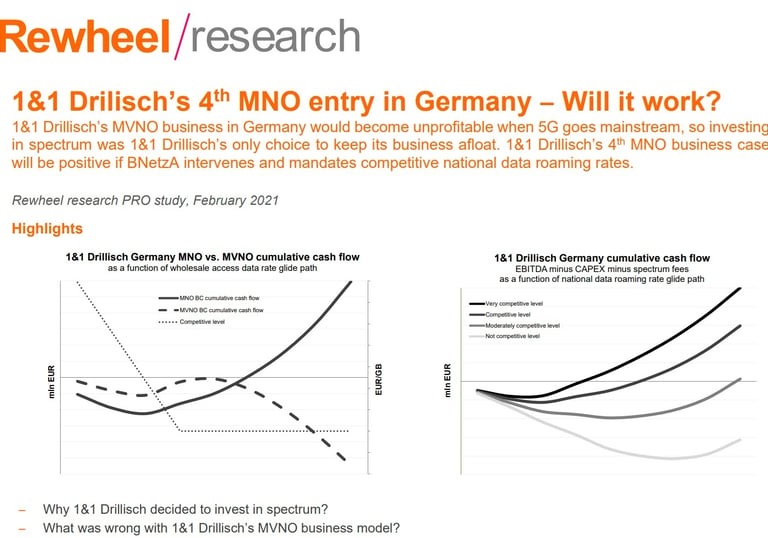

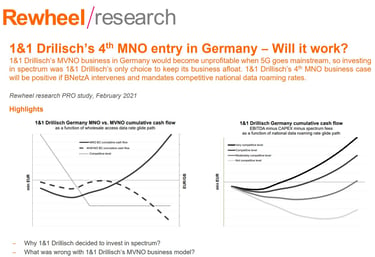

1&1 Drilisch’s 4th MNO entry in Germany ̶ Will it work?- 2021

1&1 Drillisch’s MVNO business in Germany would become unprofitable when 5G goes mainstream, so investing in spectrum was 1&1 Drillisch’s only choice to keep its business afloat. 1&1 Drillisch’s 4 th MNO business case will be positive if BNetzA intervenes and mandates competitive national data roaming rates.

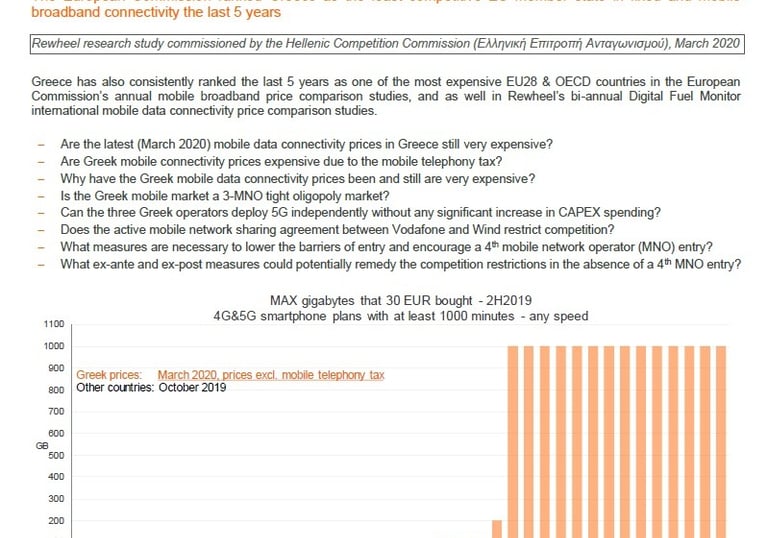

Review of mobile data connectivity competitiveness in Greece - 2020

Rewheel research study commissioned by the Hellenic Competition Commission (Ελληνική Eπιτροπή Ανταγωνισμού), March 2020. Greece has also consistently ranked the last 5 years as one of the most expensive EU28 & OECD countries in the European Commission’s annual mobile broadband price comparison studies, and as well in Rewheel’s bi-annual Digital Fuel Monitor international mobile data connectivity price comparison studies.

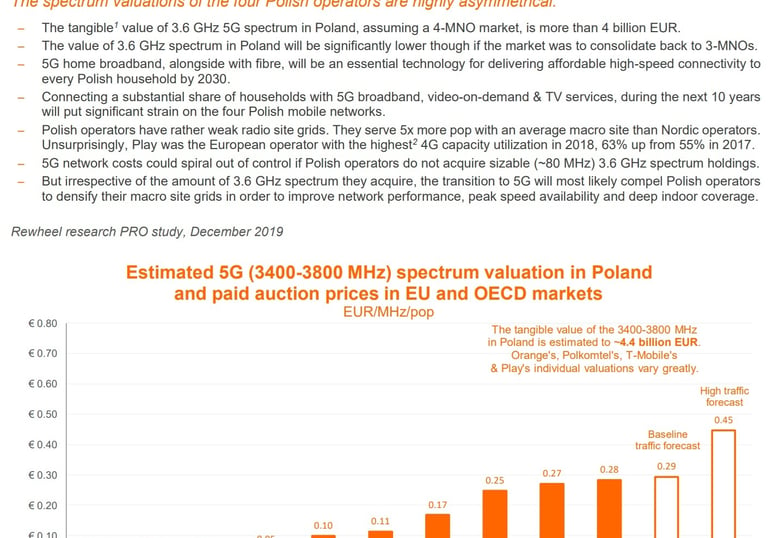

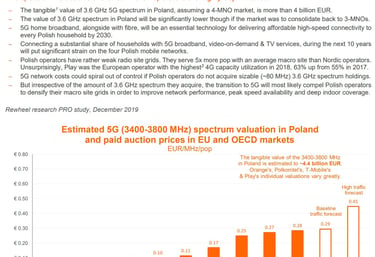

The value of 3400-3800 MHz 5G band is substantially higher in Poland than in other large EU markets. The spectrum valuations of the four Polish operators are highly asymmetrical.

3.6 GHz 5G spectrum valuation in Poland - 2019

Root cause of weak competition in the Canadian wireless market - 2019

The Canadian wireless market is ruled by provincial mobile network duopolies and monopolies. While in some provinces regional operators increasingly challenge the incumbents, at the national level, Canada is a de-facto network duopoly.

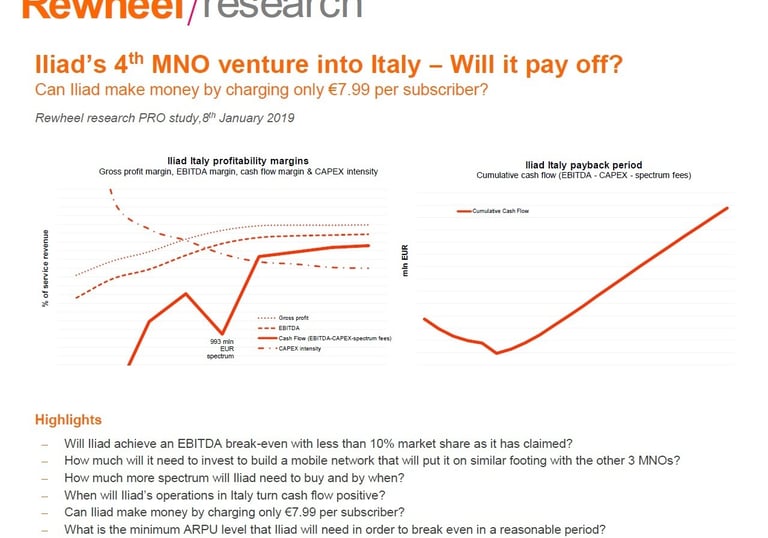

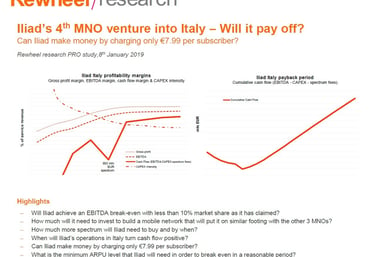

Iliad’s 4th MNO venture into Italy ̶ Will it pay off? - 2019

Can Iliad make money by charging only €7.99 per subscriber?

Has Tele2’s 4th MNO entry into the Dutch mobile market led to lower prices? ̶ Did the approval of the 4 to 3 mobile mergers in Austria, Ireland and Germany lead to higher prices? ̶ Will the proposed 4 to 3 merger of T-Mobile / Tele2 lead to higher prices and/or consumer harm?

T-Mobile and Tele2 4-to-3 mobile merger in the Netherlands – Competition concerns, network efficiencies and effective remedies - 2018

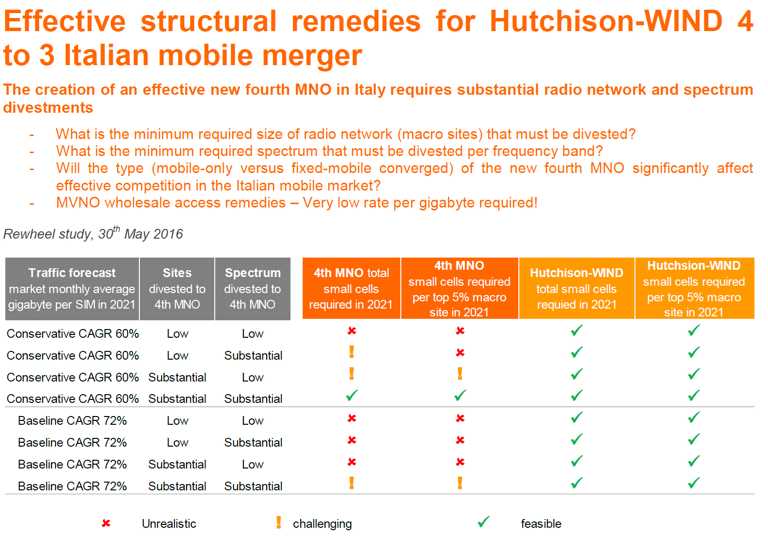

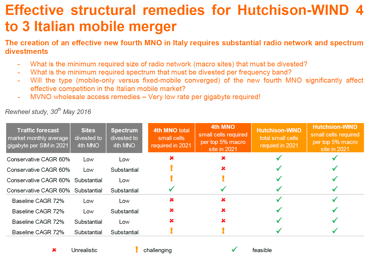

Effective structural remedies for Hutchison-WIND 4-to-3 Italian mobile merger - 2016

This research report was submitted to Commissioner Vestager and DG Competition on 30th May 2016, three months prior to the European Commission's announcement (link) of approving the merger subject to remedies.

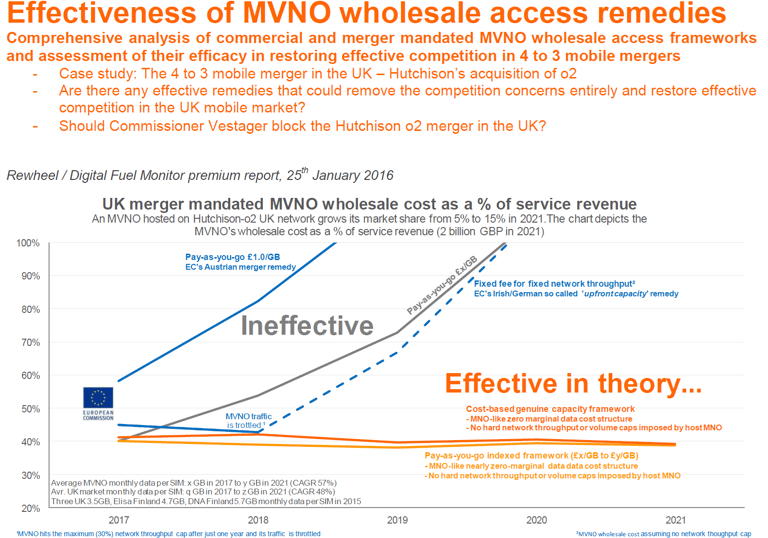

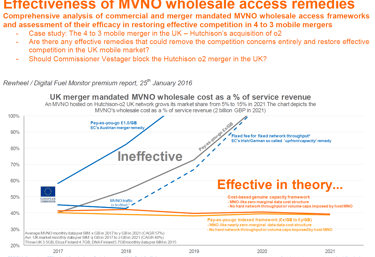

Effectiveness of MVNO wholesale access remedies - 2016

Comprehensive analysis of commercial and merger mandated MVNO wholesale access frameworks and assessment of their efficacy in restoring effective competition in 4 to 3 mobile mergers.

In its report ‘Assessing the case for in-country mobile consolidation’, prepared for the GSMA, Frontier Economics claimed “...that there is no evidence that prices increased following the merger” in Austria. According to Frontier’s dubious methodology unit prices fall even when consumers are asked to pay more Euros every month to purchase the same amount of goods. The fact is that before the merger, in December 2012, Austrian consumers paid €11 to purchase a smartphone plan with at least 1,000 minutes/SMS and 2 gigabytes. By February 2015 the price has doubled to €22.

The dubious consolidation economics of Frontier Economics - 2015

Click the image above to download a pdf list of Rewheel's research studies between 2010-2024 and get in touch if you wish to gain access to any of the studies listed in the archive.

The following authorities have acquired access to Rewheel's research: The European Commission Directorate for Competition, the United States Department of Justice, the New York, California and many other US State Attorney General Offices, the national competition authorities of Canada, Australia, the Netherlands and Greece, the Ministry of Economic Affairs of the Netherlands, the Ministry of Industry and Trade of Czechia, the Korean Electronics and Telecommunication Research Institute, the sector regulators of the United Kingdom, Germany, France, the Netherlands, Finland, Portugal, Ireland and Members of the Canadian House of Commons.

Helsinki, FINLAND

rewheel@rewheel.fi

+358 44 203 2339

EU VAT: FI22948425

Copyright © 2009-2025 Rewheel Oy. All rights reserved